Patterned Cycles (Fast Annual, Decennial, Seasonal-Weekly, Weekly-Diurnal cycles)

The explanation of Natural Cycles module is here

There are many cycles that represent some combination of other, more common and simple, cycles. They may be called "patterned" cycles (as they aim to reveal some pattern). I would like to discuss these cycles here.

Let's start with the Annual cycle and its "derivatives". The Annual cycle itself shows how the price changes within a year. How do we calculate this cycle? Skipping all technical details, we analyze ALL available price history and calculate the averaged price movement within a year. Look at the picture below. It shows the Annual cycle for Dow Jones Industrial Index calculated for all available price history, from the year 1885 till now (June 2009):

We can see here the most typical patterns like September-October drop, Christmas rally etc. The advantage of this approach is that we can see the most typical patterns and eliminate occasional movements.

The disadvantages come from the advantages. Fighting "occasional movements", we can miss some important information. Some new Annual patterns can appear while the classical Annual cycle does not see them - simply because these patterns have not existed in the past. To handle this situation, use "Fast Annual" option. It is in Natural Cycles module:

"Fast Annual" is a version of the same basic Annual cycle. The difference is that we do not use ALL available price history to calculate fast Annual cycle We use only last %X years. As we are more interested in revealing latest pattern, we do not need all available price history.

This is Annual cycle based on the last 10 years of available price history for DJI (the red curve), together with the regular, "classical", Annual:

As you see, the Classical Annual (the blue curve) and Fast Annual (the red curve) are pretty close, though some divergence presents in December. It might be because the Christmas time now is a big economical factor (Christmas sales), while several decades ago it has been considered as a big religious holiday.

You can vary the amount of the years to be analyzed here (this is Natural Cycles module):

I recommend to tie the amount of analyzed years with the most important economical cycles - like 4-year Presidential/Kitchen cycle or 9-11 year Juglar cycle. (I use 4 (Presidential cycle), 8 (double Presidential) and Decennial patterns).

Decennial cycle is another variation of patterned Annual cycle. This cycle uses decimal patterns, i.e. to calculate Annual cycle for the year 2009, use not ALL available price history, but 1999, 1989, 1979, 1969 ... years only. Such technique is based on the assumption that some similarity might exist between all XXX9 years.

This is how Decennial cycle for the year 2009 looks like:

To calculate Decennial cycle for the year 2007, we would take into account the years 1997, 1987, 1967, .., XXX7. only.

Going further we can analyze more specific patterns, say analyze 7 years pattern. To calculate such Annual pattern for the year 2009, use only years 2002, 1995, 1988... Again, we assume that some similarities exist between all years separated by seven years difference.

In Timing Solution it is possible to calculate any annual patterns:

As in the previous case, I recommend to try first pattern periods that correspond to some accepted economical cycles (4-year Presidential/ Kitchen cycle or 9-11 years Juglar cycles).

All cycles discussed above are based on Annual cycle.

Change the base to get other patterned cycles.

We can get the variety of patterned cycles based on Weekly cycle. The classical weekly cycle calculated for Dow looks:

It says that usually Dow rises in the beginning of the week and goes down at the end of the week. This curve is obtained while analyzing almost 5000 weeks of DJI history starting from the year 1885. You may ask whether the summer weekly cycle is different than the weekly cycle for winter. This is a reasonable note, and we have incorporated this approach in Timing Solution. We do it using Seasonal-Weekly cycle.

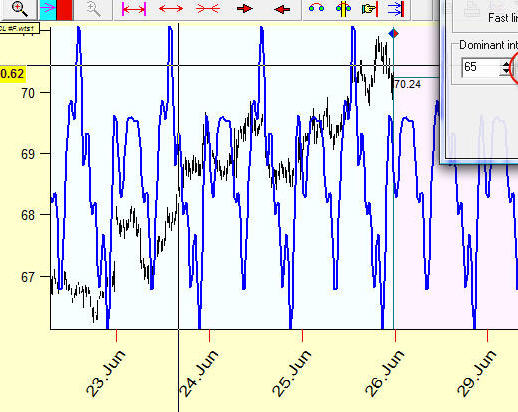

To calculate Seasonal-Weekly cycle for the current week June 21-27, 2009, we analyze not all 5000 weeks from 1885 year, we analyze June weeks only. This is how Seasonal-Weekly cycle for June looks like (together with the classical Weekly cycle):

They are close, only the maximum is shifted. The same pair for January shows a significant difference:

This is a good example why we should not consider the calendar cycles alone; they just show the most common tendency. Keep this tendency in mind and then go further. I always start any research with these basic cycles as a starting point.

The last patterned cycle I would like to consider is Weekly-Diurnal cycle. As you have already guessed, this cycle forecasts the price movements within a day, and the base for calculation is weekly data.

The classical diurnal cycles show the most common movements within specific trading days.

As an example, for Crude oil futures this cycle looks this way:

To get this cycle, we have considered all days. But you may assume that the diurnal cycle can work differently in the beginning and at the end of the week. So, exactly in the same manner as above, we can calculate five different diurnal cycles: the diurnal cycle for Mondays that analyses all intraday Monday movements till the diurnal cycle for Fridays.

Here the diurnal-Friday cycle for Crude oil futures is shown:

All these patterned cycles do provide some additional information. The key word here is "additional". For some reason, many researchers prefer to analyze it first. However, I recommend always starting with the basic cycles (Annual, Weekly) and only then consider their derivatives.