Question:

What Relative Price Oscillator

is more preferable?

Answer:

Let�s consider some chart that covers the time span of 4 years:

Here you can see the up trend movement since 2003. Looking at the details of this chart, you can see the waves that last for several months each.

Magnifying this chart for 3 months period, you can observe the price charts that take place within several days:

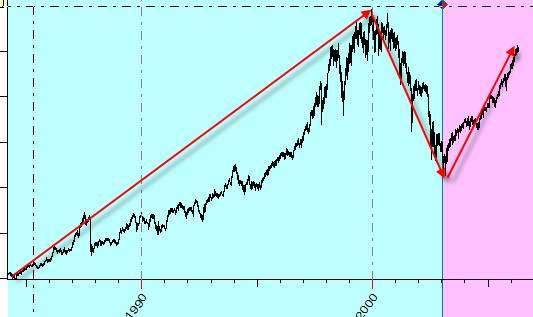

From another, side if we consider this data set in the perspective of the recent 20 years, you can see that the 2003 swing is a part of some bigger waves:

When we speak about waves inside the waves, we are referring to the fractal nature of the stock market.

When you start to make the forecast model for any financial instrument, first of all you have to decide what wave will be researched and what is the typical period of this wave. The Relative Price Oscillator (RPO) deals with this issue.

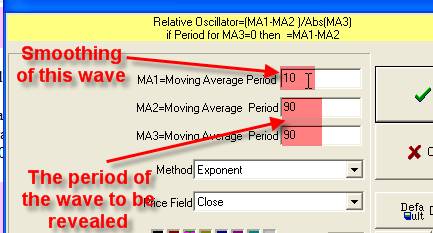

Let�s create the relative price oscillator with the period of 50 price bars. Follow these steps:

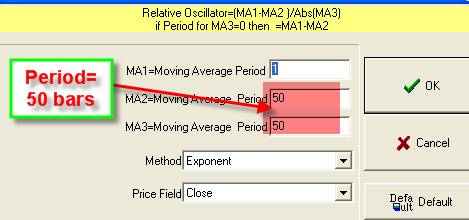

MA1, MA2, and MA3 are parameters and components of the formula for this RPO:

The� RPO(1,50,50) catches the waves that are about 50 price bars. It looks like this:

The most important feature of this oscillator is that it makes these waves horizontal. This is very important: if we look at the waves in Nature, it is much simpler to describe (and thus forecast) water waves on the lake than waves in the water flow that runs from the mountain (the mountain in this case is the analogy for the market trend).

We can make this wave smoother � if� we would like to reveal cycles that last for

several months; in this case, we are not interested in small details inside

this wave:

To eliminate small waves, we use MA1 parameter that makes this wave smoother:

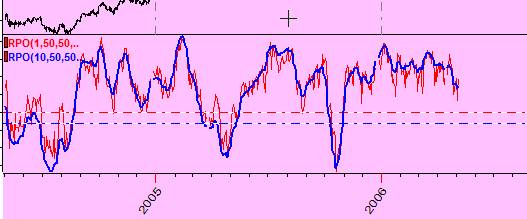

Look at these two waves together: red curve represents not smoothed oscillator RPO(1,50,50), blue line stands for smoothed oscillator RPO(10,50,50):

�

As you see, the smoothed (blue) oscillator eliminates small waves.

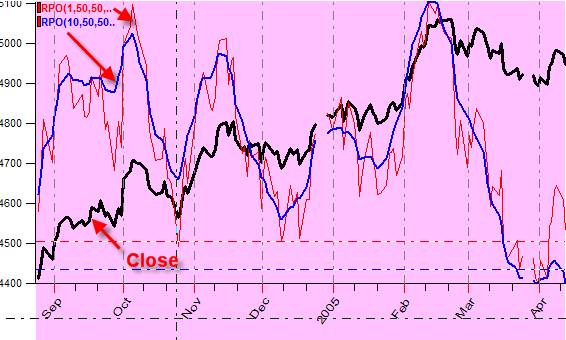

Another thing that is typical for moving averages is the lag effect. Timing Solution has a special algorithm to calculate RPO with minimized lag effect. See these lines on the same screen: a line for Close (the black line) and two different RPOs: RPO (1,50,50) and RPO (10,50,50):

�

�

The shift effect is practically eliminated.

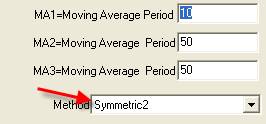

So, for practical usage, keep the MA2 and MA3� parameters equal; they define the typical period of the revealed wave, while the MA1 parameters indicates its smoothness:

Important: To calculate MA1 (the moving average), we always use the �Symmetric 2� algorithm. Thus we eliminate the lag effect typical for classical moving averages.

If you use �Symmetric� algorithms in RPO window with MA2=50 (as an example), the real period of the wave will be less than 50 price bars (due to math reasons):

,

,

However, I would recommend to use �Exponential� algorithm� here.�

The period of RPO should be compatible to the typical period of the swing that you are looking for.

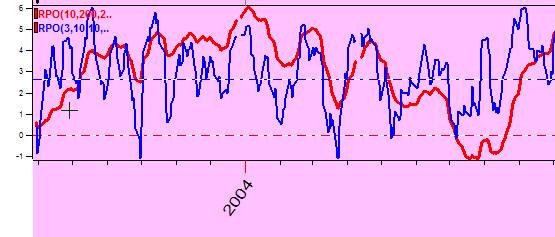

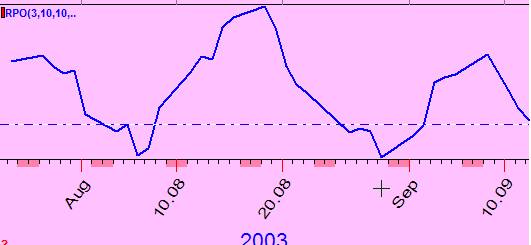

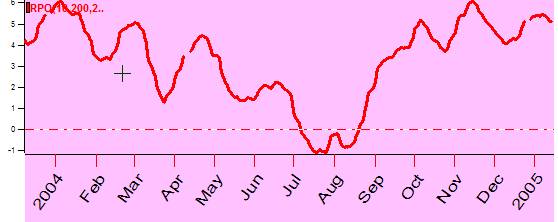

See these two RPOs displayed on the same screen: the blue line represents RPO (3,10,10) and the red line is for RPO (10,200,200):

�

�

As you see, the shorter RPO (3,10,10) sees the waves inside the month:

�while the red line represents the RPO that is more oriented to see the waves inside the year:

�

As a compromise, I often use the oscillator with 50 price bars period, RPO(1,50,50):

But you can try your own variations.

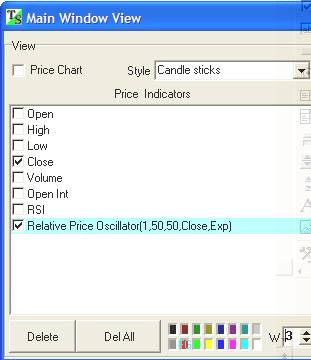

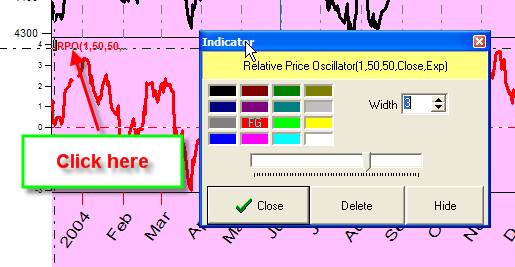

Also I would like to remind that you can change the thickness and color of any created oscillator. You can remove them as well by clicking this button:

All these operations can be performed through this window:

You can also modify the parameters of created indicators while you are in the Main window by clicking on the indicator�s identifier:

�����������

If you click this button:�

�these indicators will be used �by default�.

It means that when you download the new price chart these indicators will be

created automatically. This feature is useful if you often use the same

indicators.

�these indicators will be used �by default�.

It means that when you download the new price chart these indicators will be

created automatically. This feature is useful if you often use the same

indicators.

�����������