Naked Truth

Technique #1: Non lag moving averages (or any other indicator)

Technique #2: Adaptive RSI based on dominant cycle

Technique #3: High Annual return strategy

Technique #4: Reaction effect - trend mode versus cyclic mode

Technique #5: Saga about divergence

Why Naked Truth?

There are different forecast techniques available on the market these days. I would like to analyze some of them in this set of articles. Why do I do that? The reason is simple: TS users ask me about these techniques. I guess every month somebody out there invents something or does teaching on some exclusive method. The next day at least one of TS users asks me about that and wants to know whether it is possible to do something similar with Timing Solution software. Some questions appear again and again, year by year. So I have come up with this project. Its main purpose is to show Timing Solution users how they can verify any trading strategy and what questions they should ask to vendors/inventors of these techniques.

The idea of the project is not new to me. Actually, I have written already couple of articles regarding this issue. You will find there some valuable recommendations:

http://www.timingsolution.com/TS/Articles/beware_good_system/index.htm

and http://www.timingsolution.com/TS/Articles/bt_no_future_leaks/index.htm

In this project, I have no intention to cover all available techniques, I choose some of them that are close to the most interesting themes for me - projection line and mechanical trading systems.

Non future leaks technology - software users versus software vendors

To estimate any technology we should apply verification methods that have no future leaks. To me, non future leaks technology is as Lady Justice:

To analyze properly any trading strategy, we should wear blindfold that does not allow us to see the future - like Lady Justice that does not see who is seeking the justice. As her, we should consider only what has been done. And it is really easy to do: simply put aside a portion of price history data - and forget about it. Then conduct any research you want to, create a model, calculate your projection line and prolong it into the future. Only after that compare your forecast with this untouched piece of price data. This is a final point: as soon as you have opened your eyes (i.e., made visible this portion of the price data), you cannot change your model anymore.

Having a piece of data not participated in research and/or calculation of the projection line is the only way to put software users and software vendors in equal conditions. (Under software, I mean here any methods or techniques because practically everything today is computerized.) Observing how the forecast matches the data that were invisible at the moment of creating a forecast model, the forecast producer feels exactly the same as the user who has purchased his/her service and tries to apply it for the new coming price information.

Actually this is a very old problem between forecasters and all other people. Claiming about the future, forecasters tried to imitate the past very accurate - and often failed when the future arrived. The great Italian poet Dante Alighieri wrote about this issue 700 years ago (Inferno, Canto 20):

And I saw people in that rounding vale

silently weeping, walking at a pace

as slow and solemn as litany.

And when my eyes observed them farther down,

they seemed miraculously screwed about

between the chin and where the torso starts,

For backward to the kidneys turned the face,

and backward always did they have to go,

for they had lost the sight of thing ahead.

Maybe in wrenchings of paralysis,

a man may be so wholly twisted round,

I've never seen it, and I have my doubts.

Let us discuss some techniques.

Technique #1: Non lag moving averages (or any other indicator)

Technique description

See how good looking is a non lag moving average. There is no lag, and it "anticipates" upcoming post Crisis up trend:

This is zoomed-in picture: March 6, 2009 gives us some hope that the worst is over:

Is this indicator really good?

Solution

It is time to put a blindfold onto our eyes. Let's consider the facts. I have removed the price history information after March 6, 2009 and calculated this non lag moving average once again:

Now look again on March 6. You can see that this moving average does not "anticipate" upcoming turning point as it did on the picture above; instead, it shows steady downward move. I would say that we should not rely on this indicator only.

Technique #2: Adaptive RSI based on the dominant cycle

Technique description

a) We calculate the period of the dominant cycle (suppose in our particular case that the period of dominant cycle is 30 bars);

b) Calculate an indicator; let it be RSI with the period equal to a half of the dominant cycle's period (i.e. in this particular case it is RSI with the period = 15 bars);

c) We use this RSI as a regular Technical Analysis indicator, and from time to time we have to re-adjust it to a new dominant cycle because the dominant cycle changes all the time.

Advantage

Theoretically this kind of indicators provides the signals with a minimal lag (if the stock market is still in the cycle mode and that same cycle is still active; see the explanation below).

Good Example

Let me show this technique using one good example.

Imagine this situation: Beautiful July morning (27 July 2010); the trader opens Timing Solution software, runs Turbo Cycles module to see the cyclic portrait of S&P 500 mini futures continuous 1 min chart and receives this:

The strongest dominant cycle with the period of 30 bars plays the main role now. OK; we ask the program to calculate RSI with the period = 15 bars and watch how this RSI catches the turning points of the real time data. This is how it works:

The result is not bad at all, and we are excited as we have now some hope that this technology will work for other days.

Other Examples

The next day, on July 28, 2011, the program notifies us about the existence of 33.38 bars cycle. We calculate RSI with the period = 17 bars and watch how this indicator catches the turning points of July 28, 2011. Here it is:

We do the same on the next day, July 29: the strongest cycle is 59 bars cycle, so we have to apply RSI with the period of 30 bars. This RSI gives us these signals:

As you see, now this technology works not so good as two days earlier. The next day, Friday, brings us 56 bars cycle and leaves no hope that this technology works:

Solution

When you see a presentation of a "good" technique (as the one above), you should always ask for a dozen of consequent examples like in the pictures above. Simply ask to show how this technology works within next two weeks and watch all 10 trading days in a row.

Theory

Before going into theoretical details, I would like to show you how I chose the good example above. I simply watched at the price chart and looked for a piece of chart where the track of cyclic vibration is presented (if it is there, there will be a sinus wave in the analyzed chart). Look at this example:

Do not think about the trend now, just watch the vibration around the trend line. Some cycles may be skipped, this is not important as well. The most important thing is how major turning points are described by this harmonic wave. Look how our 30 bars wave describes major turning points:

These periods are called cyclic mode - the stock market is in cyclic mode then. All cyclic models (any of them) work very well when the stock market is in cyclic mode, and they stop working when this cyclic mode is over. It does NOT matter what techniques you apply: adaptive RSI, adaptive moving average crossover, huge variety of cyclic indicators. All these techniques work till some track of the very much desired sinus wave is presented in the financial data.

According to John Ehlers, the stock market is in cyclic mode approximately 30% of the time. We can tell whether the stock market is in this mode or not. Unfortunately, nobody can tell when this cyclic mode ends. This is Achilles' heel of any cyclic model applied for tough stock market conditions.

Timing Solution approach

Cyclic theory comes from physicists (BTW I am a physicist too). Usually the physicists deal with persistent cycles - like Lunar effect of F2 ionization researched by Julius Bartels in 1950s (http://www.timingsolution.com/TS/Links/sdarticle.pdf). Accordingly Bartels significance criteria were developed for these physical problems. It was reasonable to do as these problems are related to the phenomena that work now the same way as they worked 1000 years ago. In other words, the physicists developed these criteria to research fundamental phenomena..

When we deal with financial data, we enter the totally different World. The main rule of this World can be expressed by the words of great Greek philosopher Heraclitus 2500 years ago: "You cannot step twice into the same stream". The cycles appear and disappear; while the cycle is active, we can use it to make a forecast. After some time this cycle loses his energy and disappears. It means that our task is to find out when the new cycle appears, as early as possible. "Freshly" appeared cycle is the best tool for forecasting. We should also care about the moment when the cycle disappears.

It is true that Timing Solution software allows to reveal dominant cycles. However, our main goal is to catch "freshly" appeared/burn cycles, and it needs a different approach. I think it is better to use wavelet analysis for that purpose. This is how the wavelet diagram for our 1 minute chart looks:

The bright zones show the periods when %X cycle is active. For example, on July 27, 2010 the 31-bars cycle was very active, though after 2 pm it stopped working. You can also see how other cycles appear. This detailed wavelet diagram shows that this 31 bars cycle has appeared on July 27, at 2 am and stopped working July 27, 2 pm:

You can drag and drop this cycle on the price chart, and the program will calculate the projection line based on this cycle. This approach is explained here: http://www.timingsolution.com/TS/Study/Classes/wavelet.htm

In other words the main issue here is not revealing dominant cycle, the main issue is revealing as early as possible the moment when this cycle starts working - and handle the moment when this cycle is losing its energy. It seems to me that we should add to the picture here the fundamental analysis. Everyday the stock market is affected by lots of different factors. The short-living cycles that we discussed above may be the reaction of the stock market to these factors (it is similar to the rounds on the water when you throw there a stone). It might be that some specific cycle is a response to some specific group of factors. It needs a very special research that should involve grouping of the fundamental factors in different ways. I have heard that a similar type of research is done (or is going now) for political factors. We are not doing this research yet, we are only making ourselves ready for that ("we" stands for a really small research group that I am dealing with).

These ideas are a heart of multiframe spectrum, a technique I am developing for more than 10 years now. The central parameter here is stock market memory (briefly sm), it shows the life (or longevity) of %X cycle. According to my research, for most markets the stock market memory varies in the range of 3-15. Within this short period we can consider our models as stable models and apply the classical spectrum theory for that. You can consider multiframe spectrum as the extension of the classical spectral analysis applied to very unstable data. Last year I also worked on another variant of cyclic analysis - quantum approach.

Dominant cycle definition

There are several definitions of a dominant cycle. This issue is explained in this article: http://www.timingsolution.com/TI/2/index.htm

Here you can find two worksheets; one is for the example that I used in this article and another example was asked by some user:

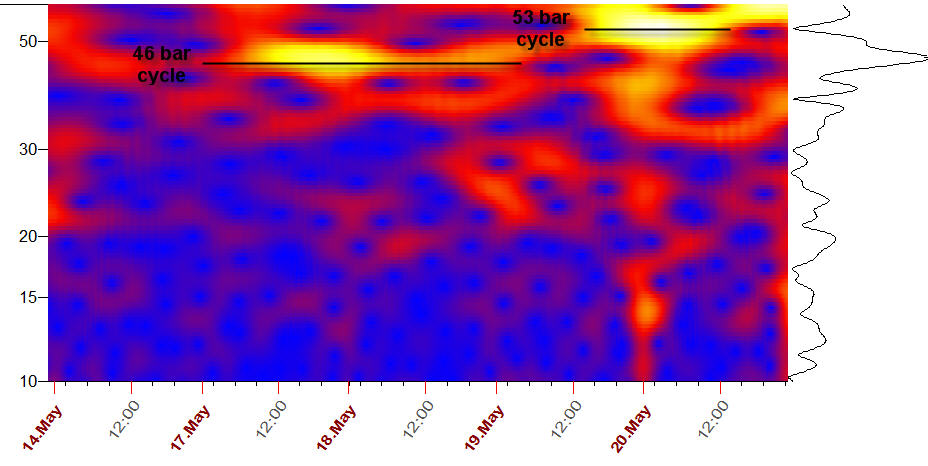

It shows the strongest cycle and the wave based on that 46-bars cycle (run Turbo Cycles, set First 1 cycles, amount overtones 1, set to LBC May 17 2010 ), plus RSI 23.

This is a wavelet diagram for this period:

46 bars cycle was active during 2 full days: May 17-18. This is a good cycle, tradable. On May 19-20, another 53 bars cycle, a very strong one, has appeared though it did not live too long.

Technique #3: High Annual return strategy

Technique description

This is my own research: http://www.timingsolution.com/TS/Articles/trading_signals/index.htm

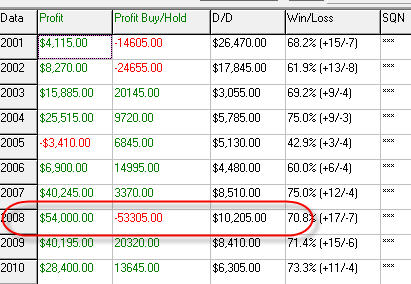

There is one trading strategy that gives 54% Annual return in the hardest 2008 year:

It looks good. However I feel myself uncomfortable dealing with this high percentage, and I will explain why.

Solution

Check all trades one by one for the year 2008 to figure out how the money is made.

In total we have 24 trades during this period.

Look at the most profitable trades:

Close short February 5 gives us 16K profit

Close short September 15 - $8.8K

Close short September 29 - $9.5K

Close short October 15 - $11.3K

Altogether is $45.5K.

In other words 80% of the profit is provided by 4 short trades, 4 of 24 (i.e 15% trades). Personally, I feel myself very uncomfortable with this strategy. This is a true gambler strategy - make one good trade and do anything you want after that. The analyzed strategy is still good, and there is a reason for these sky high %: it is a result of the highly volatile stock market in 2008 and nothing more. I would be very cautious with these high % .

In the first version of Trading Strategy Module I simply ignored these extreme trades, then users started screaming about non-consistent digits (like profit factor) that did not fit Excel and other programs, so I had to returned to classical calculations.

Technique #4: Reaction effect - trend mode versus cyclic mode

Technique description

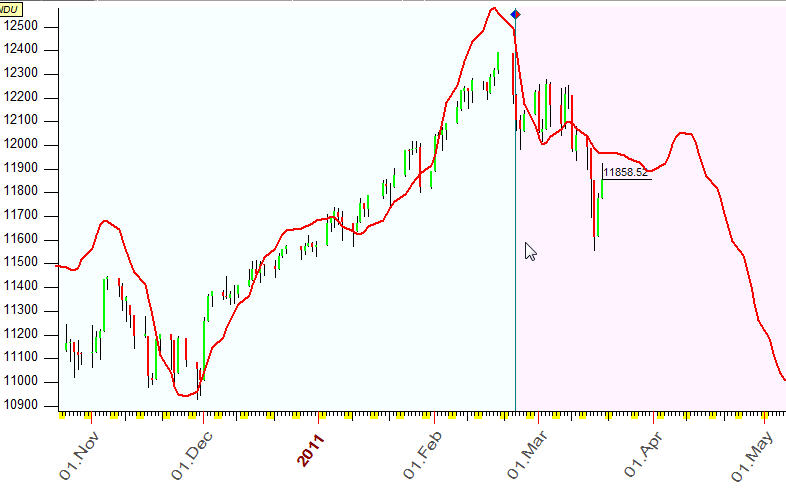

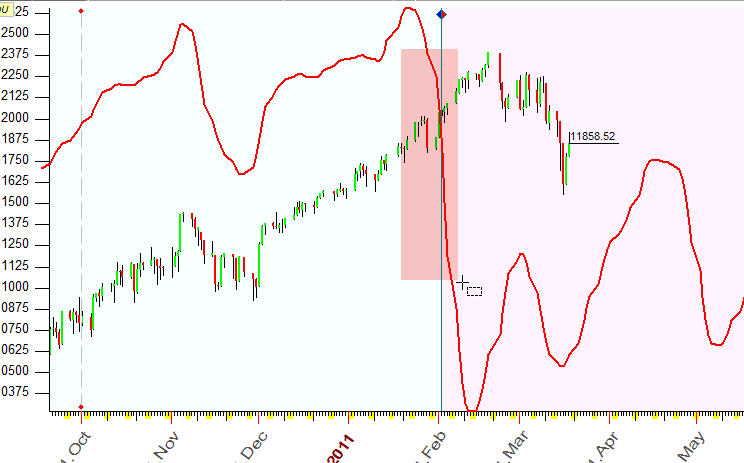

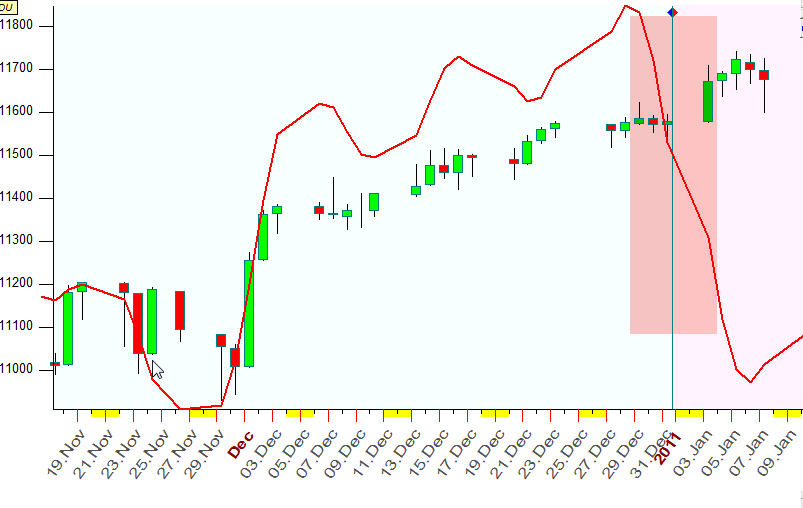

Every time when the stock market changes the trend we always hear that somebody has forecasted this turning point. However it neither proves nor disapproves the models that they applied for the forecast. I would like to show how to verify these models. As an example the last turning change in trend point (February, 18 2011) will be analyzed. Here you can see the model that "forecasts" this drop:

This is a cyclic model (Turbo Cycles module). In other words if you would follow this model on February, 18 2011, you would win. Could we follow this advice? The answer is - No.

Solution

To answer this question we need to perform the simplest back testing procedure. Let's ask yourself: what has our model advised to us in the beginning of February 2011? Here it is:

You see, this modes has shown a sharp and immediate down, while in reality we had two weeks of up trend movement. The important fact is - to calculate this projection line we used the price history data prior to February, 2011 only (not all data that we have now, in March). Doing this, we put ourselves in the position that is maximally close to the reality; this is a core idea of non future leaks technology. If it would be a model that really could do that forecast, we would see it.

Now we try to do the same using the price history till the beginning of January 2011. And we have the same story:

In other words if one beautiful winter morning, since January till the middle of February, you would run that Turbo Cycles model to get some ideas regarding next weeks movements, I guarantee - the projection line would show you downward.

Why? Look at the price chart since December 2010. We have a strong and steady up trend:

Any model that is based on cycles will show you that this trend movement will stop son, and the correction will start. This is a restriction of ANY cyclic model; this is a natural response of the cyclic model to the trend, a cyclic model's reaction. You can find more info about the reaction effect here: http://www.timingsolution.com/TS/Study/Reaction/reaction.htm

To check any model in regards to the reaction effect, I recommend to vary Learning Border Cursor (LBC) with the right mouse click and watch the projection line after LBC:

Technique #5: Saga about divergence

Technique description

This is a very often used approach, I think this is the most popular technique in Technical Analysis. Here is the example: we calculate RSI (relative strength index). According to Classical approach, we would watch the moments when this indicator breaks overbought/oversold levels and especially when there is divergence between RSI (points down) and the price itself (points up) like this:

They state: the existence of this divergence is a reliable indicator of upcoming turning point.

Solution

Simply watch how this approach works for big amount of examples (let's say watch for a dozen of turning points) and you will see.

Theory

This is practically the same problem as reaction effect for cyclic models explained in the previous section. All non trend indicators - like different oscillators, momentum, RSI, MACD and many others, - assume the existence of some eternal regular cyclical movement in the price behavior. We define the window for RSI indicator, smoothing period for relative price oscillator, etc. For example RSI with window 28 bars assumes the existence of 56 (2X28) bars cycle. If for some reason the price does not follow this 56 bars cycle and continues its up trend movement without any significant correction, RSI index becomes being flat or even moves against the price (divergence). So in most cases this divergence means "malfunction" in the working oscillator, it cannot describe the stock market reality because some other cycles are playing now the main role here. Sometimes these divergence zones can coincide with the next turning point, sometimes not, like this one:

Actually all indicators based on dominant cycles (like adaptive RSI) have been developed to handle the situation when the cycle that lies behind the indicator and real dominant cycles that rule the stock market are different (and this discrepancy causes divergence). Instead of divergence we should deal with the oscillator that switches onto a more longer wave while the stock market is in trend mode (trend as a part of a longer wave). But it looks like this approach does not work as well. In any case in most cases divergence means disadvantage of some system, not its advantage.